Why There Will Be No Stable Post-War Order After the End of The War Over Ukraine

Tomasz Konicz

Is this the big one? Is this the big crash that will overturn everything that has been established in global structures and dynamics since the breakthrough of neoliberalism in the 1980s? The war over Ukraine could indeed be seen in retrospect as an epochal break, as a tipping point in the global crisis process, at the crossing of which the crisis of the late capitalist world system has taken on a new quality.

That the world capitalist system is in a severe systemic crisis,[1] after decades of ignorance and marginalization[2] value-critical crisis theory, is now generally accepted even on the German left, but the character of the crisis process still seems to be only partially understood. For the late capitalist systemic crisis is not a one-off event, not merely a “big crash,” but a historical process that unfolds in spurts over decades, eating away from the periphery into the centers of the world system. The debt crises of the Third World, which in the 1980s marked the beginning of the now collapsing neoliberal era and left behind a series of civil wars and “failed states,” have long since spread to the centers of the world system. This is evident, for example, in the increasing tendencies towards stagflation, which are reminiscent of the stagflation period in the 1970s – which at that time helped neoliberalism to achieve its breakthrough.[3]

The systemic crisis is therefore not a “big crash,”[4] but rather a historical process of increasing internal and external contradictions of capital, which, due to competition-mediated rationalization, gets rid of its own substance, the value-creating labor of commodity production[5] and leads to an ecologically devastated world.[6] This historical process of crisis, which gave rise precisely to neoliberalism as a system of “delaying the crisis,” is characterized by phases of latency interrupted by manifest waves of crisis in the centers: such as the dot-com bubble of 2000, the real estate bubble of 2008, the pandemic-induced crisis of 2020, and the upheavals now beginning with war. The crisis was delayed at the expense of increasing instability of the system, which had to cope with ever more violent waves of crisis in the neoliberal decades, and the accumulation of crisis potential.

The Dialectic of The Crisis

The episodes of crisis that gain in intensity and in which the crisis becomes manifest are thus preceded by a long latent phase in which the crisis potential resulting from the self-contradiction of capital accumulates, mostly in the form of rising mountains of debt or financial market bubbles,[7] which still allow the hyper-productive system a kind of zombie-like illusory life through credit-financed demand[8] – and it is precisely this debt tower construction that is reaching its inner limits due to the current inflation dynamics.[9] The quantitative process, the accumulation of debt and the rise of speculative bubbles, leads, after crossing a tipping point, to a qualitative upheaval, to the outbreak of a debt crisis or the bursting of a debt bubble, which are then also publicly perceived as a “crisis.”

The same materialist dialectic of the transformation of quantitative changes into a new quality can also be observed in the capitalist climate crisis.[10][11] Here it is the quantitative increase of greenhouse gases in the atmosphere that leads to a fundamental, qualitative change of the climate system once certain tipping points are passed. (Incidentally, the habituation effects that occurred between the economic or ecological waves of crisis also promoted crisis ignorance, since the consequences of a crisis in the centers or the periphery very quickly sedimented into a new “normality” in the ahistorical public).

The financial market-driven neoliberal variant of capitalism, which took hold in response to stagflation and the end of the great post-war boom in the 1970s, has to a certain extent run capitalism “on credit” in both economic and ecological terms. Since the 1980s, the global debt burden has been rising faster than world economic output, leading to ever stronger financial market quakes in the form of speculative bubbles and debt crises. And ecologically, too, neoliberal capitalist globalization has been accompanied by steadily rising CO2 emissions, which so far could only be reduced in the short term at the price of economic crises. And it is precisely the increasing climatic and economic distortions that make the system in its neoliberal form increasingly unstable.

The neoliberal debt tower construction that is the foundation of this era cannot continue ad infinitum. The same is true of the fossil fuel driven world combustion engine (Weltverbrennungsmaschine),[12] brought about by neoliberal globalization, which is, in effect, a globalization of debt dynamics. The quantitative increase in the potential for crisis, which has created a global debt mountain equal to 356% of world economic output[13] and a CO2 concentration of 419.82 ppm,[14] is leading capitalism to its inner and outer limit, at least to the developmental limit of the neoliberal era of capital. A qualitative shift into another form of capitalist crisis management seems inevitable (overcoming the economic and ecological crisis of capital is impossible within the framework of the capitalist social formation).

This dialectical shift from quantity to quality takes place in particular with regard to the process of globalization, which seems to be turning into its opposite. It is precisely here that the outlines of a new phase of crisis are clearly emerging, which would be characterized by a “fragmentation of the world economy into geopolitical blocs,” in which “distinct technology standards, cross-border payment systems, and reserve currencies” would be used, as the International Monetary Fund (IMF) warned in a paper in April 2022.[15] As early as mid-March, the IMF described the war as a “severe blow to the global economy” that would not only “fundamentally alter the global economic and geopolitical order” but would also be accompanied by the risk of increased instability in peripheral regions such as Africa or Latin America, which would be affected by growing food insecurity.[16]

De-Globalization

The war-related sanctions are disrupting important global trade flows and causing rapid price increases not only for energy but also for food, since Russia, Belarus and Ukraine are among the world’s most important exporters of grain and fertilizer.[17] In the case of essential goods, food and fossil fuels, capitalist globalization has already effectively collapsed. Western sanctions on Russian and Belarusian fertilizers are likely to reduce agricultural production in many countries.[18]

But it is not only the imperialist front between East and West in the Ukraine war that is contributing to the price explosion – even uninvolved countries have long since resorted to protectionist measures to ensure food security and domestic political stability. Due to massively rising prices and the threat of supply shortages, Indonesia, for example, issued an export ban on palm oil, which further exacerbated the supply situation, especially in the global South, as the war had already caused exports of Ukrainian sunflower oil to collapse.[19] India acted similarly with its recent export ban on wheat.[20]

The inflation and supply shortages that were already occurring before the war due to the pandemic are now gaining force in the context of the de-globalization that is abruptly taking hold. But even this big bang, shaking up global flows of goods and finance, is not coming out of the blue. Efforts to revise globalization have been virulent for years, especially in the form of US President Donald Trump, who personifies the contradictions of capitalist commodity production like no other. Elected by sections of the pauperized US middle class, Trump set out to make a deindustrialized America, plagued by a gigantic trade deficit, “great” again – by erecting trade barriers. The goal of Trump’s protectionism: a reindustrialization of the United States.

The debt dynamics that developed during neoliberal financialization, which set in after the end of the great post-war Fordist boom and left the world system increasingly running on credit,[21] did not develop uniformly. There were regions with large deficits, such as the USA or southern Europe, and countries with large export surpluses. This led to the formation of deficit cycles, which became increasingly important during globalization and shaped the course of the episodes of crisis in the first two decades of the 21st century (real estate bubble, Euro crisis). Globalization, and its accompanying disruptions, is thus obviously not the cause of the capitalist crisis process, such as financial market bubbles and debt crises, but is its historical course.

The largest deficit cycle, the Pacific deficit cycle between the United States and China, was characterized by the fact that the People’s Republic, which was emerging as the new “workshop of the world,” exported gigantic quantities of goods across the Pacific to the de-industrializing United States and thus built up enormous trade surpluses, while in the opposite direction flowed a financial market flood of United States debt securities, so that China rose to become Washington’s largest foreign creditor.[22] A similar, smaller deficit cycle formed between the FRG and the southern periphery of the Eurozone in the period from the introduction of the euro up to the euro crisis.[23]

Globalization was thus not only characterized by the construction of global supply chains, but also the corresponding globalization of debt dynamics, realized through deficit cycles, which, as mentioned, have grown faster than world economic output in the past decades – and consequently functioned as a major economic engine by generating credit-financed demand. The globalization that produced these gigantic global trade imbalances was a systemic reaction, a flight forward from the increasing internal contradictions of the capitalist mode of production, which is choking on its own productivity.

What is now unfolding globally could be studied in rudimentary form on the basis of the euro crisis: As long as the mountains of debt grow and the financial market bubbles are on the rise, all the states involved seem to profit from this growth on credit. But as soon as the bubbles burst, the battle over who should bear the costs of the crisis begins. In Europe, as is well known, Berlin has used the crisis to pass on the costs of the crisis to southern Europe in the form of Schäuble’s infamous austerity measures. Now, at the global level, the collapse of the much larger debt-financed deficit economy, which has most recently been kept alive primarily by the central banks’ expansionary monetary policy, is imminent.

The value accumulated in the financial sphere, the “fictitious” capital not generated by the valorization of labor power, will be devalued due to the absence of a new accumulation regime in commodity production.[24] The increasing inflation, in the face of which bourgeois monetary policy finds itself in a crisis trap,[25] is precisely the expression of the inevitable devaluation of value. For many states that were previously chained to globalization by means of deficit cycles and in locational competition, the increasing costs of the crisis exceed the eroding advantages of deficit cycles, so that national and regional centrifugal tendencies gain the upper hand and force the collapse of globalization. This is a crisis-induced contradiction. Capitalism is full of them.

China as The New Hegemon?

It is precisely this exhaustion of the neoliberal debt tower construction of the past decades that has the late capitalist state monsters increasingly seeking refuge from the escalating internal contradictions in external expansion. Turkey, plagued by high double-digit inflation and driven by Erdogan into ever new imperialist campaigns of conquest, is only the blueprint, so to speak, for the manifest crisis imperialism that is rampant in many places. This crisis-driven, neo-imperial flight to war is also evident in the case of Russia, which had to put down a number of uprisings and unrest in its post-Soviet “backyard” in the months before the invasion of Ukraine.[26]

But this causal link between crisis and war is also manifested in the expansive actions of the West in the post-Soviet space, which, with its refusal to agree to neutrality guarantees for Ukraine, clearly provoked the Russian war of aggression in the Kremlin’s geopolitical “backyard.” For the United States, the struggle against Eurasia, as indicated by the alliance of China and Russia, is a struggle for hegemony and the US dollar in its function as the world reserve currency.[27] The United States, because of its extreme trade deficit, acted in a sense as a black hole in the world economy, absorbing much of the surplus production of hyper-productive late capitalist industry. With inflation rapidly accelerating, fueled, after all, not only by the expansionary monetary policies of central banks, but also by resource constraints and the full-blown climate crisis,[28] Washington’s ability to borrow freely in the world’s reserve currency, the measure of value of all things commodity, is on the line.

At the same time, for China, which together with Russia is striving to form a Eurasian power bloc, the looming end of the US deficit economy removes an important incentive to tolerate US hegemony: The extreme Chinese export surpluses, which in the 1990s and at the beginning of the 21st century contributed significantly to the recuperative capitalist industrialization of the People’s Republic, have not played a central role as an economic driver since the outbreak of the real estate crisis in 2008 – and they are also likely to lose weight rapidly vis-à-vis the USA in the future.

And yet it is a fallacy to interpret the current global upheaval as a transition to a new hegemonic system in which China would, in a sense, “inherit” the United States. The Middle Kingdom does appear to be in the process of replacing the United States as the global capitalist hegemonic power – but at the same time, this upheaval is no longer possible within the framework of the capitalist mode of production due to the escalating socio-ecological crisis. The history of the global expansion of the capitalist world system, which began in the 16th century, takes place in hegemonic cycles, such as those described by Giovanni Arrighi in his fascinating work “Adam Smith in Beijing”:[29] An emerging power gains a dominant position within the system, then after a certain period of dominance this hegemonic power goes into imperial decline and is finally replaced by a new hegemon.

According to Arrighi, every hegemonic cycle has two phases: First, a phase of imperial ascent takes place, characterized by a “material expansion,” i.e. by the dominance of the commodity-producing industry of the new hegemonic power. After the outbreak of an economic “signal crisis” – triggered by processes of over-accumulation – the phase of imperial descent sets in, which is accompanied by financial expansion and the dominance of the financial industry, and which once again gives the descending hegemon a final economic and imperial heyday.

And this sequence can be clearly confirmed empirically in the case of both the UK and the US. The English Empire, which rose to become the “workshop of the world” in the context of industrialization in the 18th century, transformed itself into the world’s financial center in the second half of the 19th century, before being replaced in the first half of the 20th century by the economically ascendant USA, which in turn experienced its “signal crisis” during the crisis phase of stagflation in the 1970s. This was followed by the deindustrialization and financialization of the USA, which led to the economic dominance of the financial sector.

Moreover, Arrighi argues that the alternation between two hegemonic cycles is accompanied by the descending hegemonic power becoming indebted to the ascending hegemon, as exemplified in the book by Britain’s increasing economic dependence on the United States during the First World War. Britain built up a huge trade deficit with the U.S. during the World War period, “supplying billions of dollars worth of munitions and food to the Allies but receiving few goods in return.” Incidentally, Britain acted similarly in its role as “banker” to the anti-Napoleonic coalition some one hundred years earlier. And it was precisely this dependency relationship between a declining United States and a rising China that was described in terms of the Pacific deficit cycle, in which Chinese export surpluses contributed to China’s export-driven industrialization and deficit-building in the United States.

So, what is wrong here? What is wrong this time so that a new, Chinese hegemonic cycle is impossible? Why can’t the 20th “American” century be replaced by the 21st “Chinese” century? For one thing, China has obviously already passed its “signal crisis” marking the transition to a financial market-driven growth model in 2008. With the bursting of the real estate bubbles in the US and Europe, China’s extreme export surpluses (with the exception of the US) declined, while the gigantic stimulus packages that Beijing launched at the time to prop up the economy led to a transformation of China’s economic dynamics: exports lost weight, and the credit-financed construction industry and the real estate sector henceforth formed the central drivers of economic growth.

According to official statistics, China, for example, consumed around 6.6 gigatons of concrete between 2011 and 2013, which means that the People’s Republic, condemned to a permanent boom, produced more concrete in three years than the USA did in the entire 20th century. With this amount, the whole of Hawaii could be covered in concrete and turned into one huge parking lot, the Washington Post enthusiastically wrote at the end of March 2015.[30] The United States had used 4.5 gigatons of concrete in the past century, according to the WP, adding that the official figures from Beijing would also stand up to closer scrutiny – which is by no means self-evident. The figures are “surprisingly logical,” given that much of China’s infrastructure was not built until the 21st century and that urbanization in the world’s most populous country is proceeding apace. In 1978, just under one-fifth of all Chinese people lived in cities; by 2020, that figure had risen to 60 percent.

China’s growth is thus also running on credit, the “People’s Republic” is just as highly indebted as the declining Western centers of the world system (even more: China’s rise to become the “workshop of the world” was also based on debt processes in Western Europe and the USA due to Chinese export surpluses within the framework of the aforementioned deficit cycles).[31] And this Chinese deficit cycle produces far greater speculative excesses than in the USA or Western Europe, made evident by the disruptions on the absurdly inflated Chinese real estate market in 2021.[32] This lack of a new accumulation regime in commodity production, in which the inner barrier of capital manifests itself, forms the major difference between China and the US: Washington, after WW2, at the beginning of its hegemony, was able to build on two decades of coming capital expansion under Fordism. China, on the other hand, because of its collapsing towers of debt in an over-indebted late capitalist world system, looks as if it was already in decline before it achieved hegemony.

Another moment that makes a Chinese hegemony in the late capitalist world system impossible from an ecological point of view was described by Arrighi in his aforementioned work as the historical tendency towards progression within the hegemonic cycles: the territory, the population as well as the economic weight of the hegemonic powers increase in the history of the capitalist world system. From the few million subjects of Great Britain to hundreds of millions of US citizens of the continent-like hegemon USA to the last possible increment of the billion-person state China. This, however, also breaks the ecological limits of the capitalist world system,[33] since China is already the largest emitter of greenhouse gases and the climate crisis is already having catastrophic consequences.[34]

Oceania vs. Eurasia?

The collapse of the global deficit economy and the escalating climate crisis stand in the way of a new “world order” shaped by Beijing, a Chinese hegemonic cycle. Hegemony, after all, means that the position of the hegemon is at the very least tolerated, since it is accompanied by advantages for the other states in this hegemonic system. In the case of the US, it was the long post-war Fordist boom and – from the 1980s onwards – the deficit economy based on the world’s reserve currency, the dollar, that enabled Washington to achieve hegemony. China’s rise, by contrast, can no longer be based on such an economic foundation.

The historical hegemonic cycle of the capitalist world system is thus superimposed on the socio-ecological crisis process of capital, it interacts with it and allows China’s hegemonic rise and disintegration to merge. In place of the US hegemonic system, which went into open dissolution with the invasion of Iraq from 2003 onwards, there now seems to be a global bloc formation, in which Eurasia (Russia and China) and Oceania (USA together with its Atlantic and Pacific alliance systems) are in a perpetual conflict in a real dystopia. Yet even this frontline position, reminiscent of the Cold War – which escalated into open conflict in Ukraine – is likely to remain unstable and volatile. It could even be argued that Washington and London, as the driving forces in the Ukraine conflict, are also pursuing the goal of welding together the eroding Western alliance system through a common front against Moscow in the trenches of eastern Ukraine.

The collapse of globalization is synonymous with the collapse of the global deficit economy outlined above, which stabilized the world system in the neoliberal era. This is the decisive factor that will shape the further course of the crisis. The debt tower construction, which was maintained by means of money printing by the central banks and which delayed the manifest outbreak of the crisis in the neo-liberal period, is just collapsing, without a new accumulation regime in sight, which results in the intensification of blind crisis competition at all levels of capitalist socialization. A “post-war order” hardly seems possible any more, due to the increasing impacts of the crisis and the thus increasing crisis competition.

This also applies to crisis imperialism, which, while evoking memories of the 19th century, is driven by an inverted logic of development. While the first imperialist “Great Game” took place in a phase of global expansion of capital, in which ever new peripheral regions were integrated into the capitalist world system by means of fire and sword, its re-enactment in the 21st century takes place against the backdrop of the contraction of the valorization process, which leaves behind more and more economically and ecologically “scorched earth” along with the corresponding “failed states.”

In a nutshell: Since capital can no longer continue its zombie life financed on credit, the late capitalist state monsters are falling over each other, making all current alliances unstable, since the crisis-related competitive pressure is also increasing between the EU and the USA, between Beijing and Moscow. There is a certain inevitability in all this, since the striving for international standing in the world crisis of capital is in fact tantamount to a fight against social and economic decline, a fight on the Titanic of the late capitalist world system, which is in the process of open decay. Exclusion of the economically superfluous and the securing of resources are central moments of this crisis imperialism, while the inferior powers and world regions stagger into state collapse.

This becomes particularly clear in the example of the war over Ukraine, where both sides are in fact endeavoring to instrumentalize tendencies towards state disintegration for their own interests. Moscow is working to establish loyal “people’s republics” in the occupied Russian-speaking regions of Ukraine – following the example of Donetsk and Luhansk – in order to be able to incorporate them into the Russian Federation. Ukraine’s far right, on the other hand, which currently forms the fanatical spearhead of the Ukrainian military, sees the war as an opportunity to accelerate Russia’s state disintegration in order to realize imperial ambitions in its slipstream.[35]

It is a Taliban logic that is unfolding here, in which – similar to Western military aid to Afghanistan’s holy warriors in the 1980s – an extremist movement is being ramped up that will destabilize the region as the crisis progresses and bring the already anomic tendencies in the rotten Ukrainian state apparatus (which is just as corrupt as Russia’s) to full fruition. The Nazis of Ukraine, who are currently gaining influence at a rapid pace[36]– similar to the crisis imperialism described above – only superficially follow their historical model. Having set out to fight for the classic national empire in the form of a state, they are in fact the subject of the anomic barbarism objectively unfolding in the course of the crisis, i.e. of the rapidly advancing decay of the state.

Another moment of the new phase of the crisis, in which the external and internal barriers of capital interact, is also becoming clearly discernible during the Ukraine war: the rapidly spreading shortage of resources and food, which, although currently sold as a consequence of war, will turn into a permanent phenomenon.[37] The late capitalist global agrarian system, which has turned humanity’s natural resources and livelihoods into bearers of value and is burning them for the purpose of rampant value valorization,[38] is unable, in the face of the escalating climate crisis and collapsing globalization, to sustain the food supply for large segments of humanity on the periphery of the world system – even though this would still be possible in a resource-conserving post-capitalist system, despite the escalating climate crisis.

With the ever more clearly emerging collapse of the global deficit economy, including the deficit cycles described above, and with the devaluation of value that is now also imminent in the centers, both in the euro and the dollar area, and which is in all likelihood being heralded by stagflation, global supply chains for raw materials, resources and basic foodstuffs are also likely to collapse or at least be severely damaged. The crisis of scarcity characteristic of the new quality of the crisis, which is already spreading in the periphery,[39] is thus a product of the escalating contradictions that are inherent in the growth compulsion of capital – and here, too, the “supply bottleneck” under which German industry, for example, is groaning, was only the manifestation of this new quality of the crisis of a world system that is moving into open disintegration in the course of the pandemic.

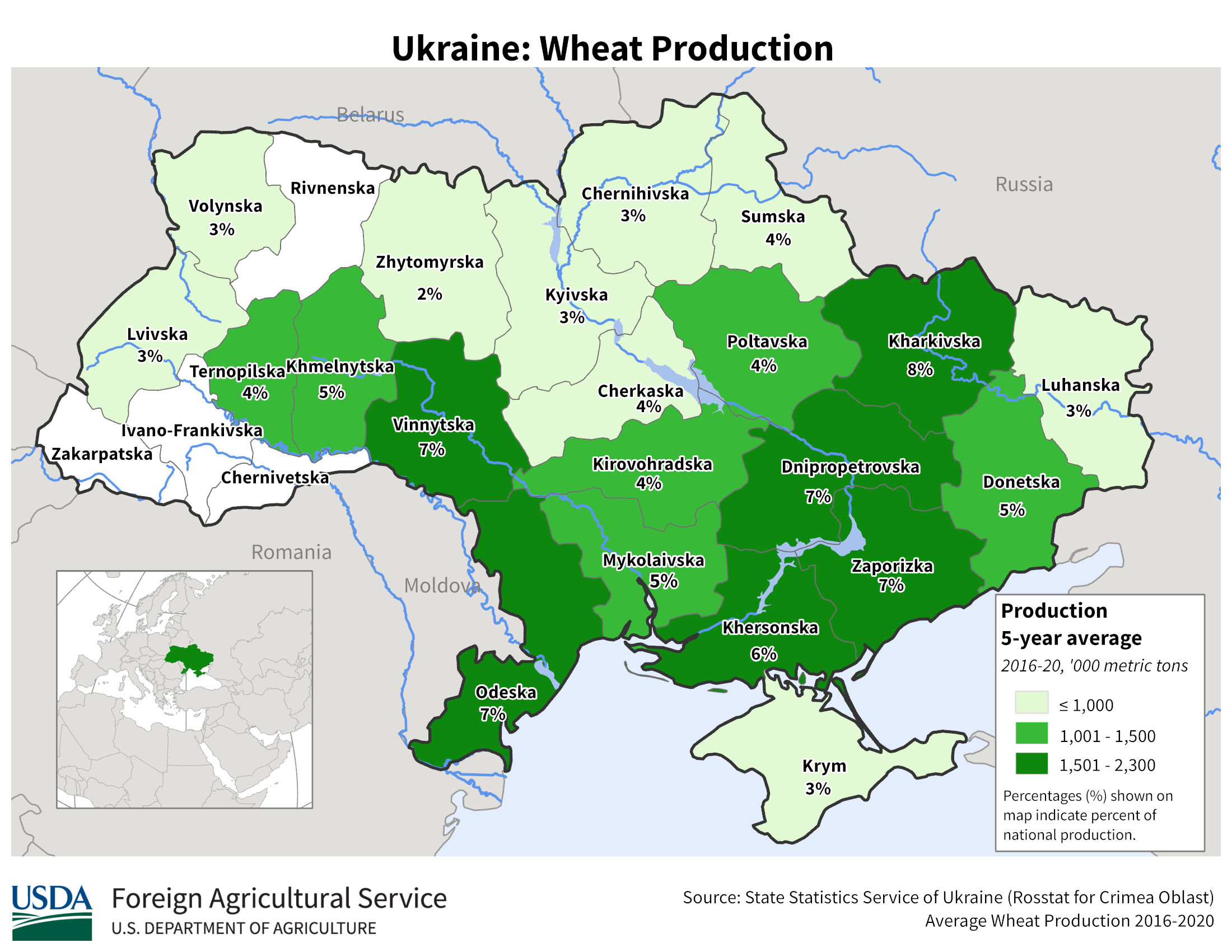

The character of the neo-imperialist “Great Game” over Ukraine has changed since 2014 – when the West intervened[40] to prevent the formation of the “Eurasian Union” propagated by Putin. With the battle over Ukraine’s southern and southeastern regions, which the Kremlin wants to incorporate into its rotten empire, an archaic-looking resource war is now also taking place. These swaths of land have the highest agricultural yields.[41] Moscow, which has failed to modernize the Russian economy, is thus expanding its strategy of an “energy empire,” which seeks extensive control of the “value chain” of energy resources, to include other “scarce” resources: basic foodstuffs. Russia not only wants to be a nuclear-armed gas station, it also wants to be a granary – precisely in anticipation of the climate crisis.

The Russian invasion of Ukraine thus provides a glimpse of the coming period of crisis, in which a capitalist world system in the process of disintegration will no longer allow for a fixed hegemony or bloc formation due to increasing economic and ecological devastation, while openly warlike confrontations over essential resources are likely to increase, even between the great powers that are increasingly sealing themselves off from the periphery. In a sense, everything will become oil – especially since the crisis process does not adhere to the reified form in which it appears in bourgeois crisis discourse, and the individual moments of this dynamic, which are separated in public discourse into “economic crisis,” “climate crisis,” “political instability” or “supply shortages,” will increasingly interact with each other. The vanishing point of this new quality of the crisis on a geopolitical, “neo-imperial” level is ultimately the nuclear exchange of blows, which is becoming more and more likely with the increasing intensity of ecological and economic crises, with ever new, more violent “crisis impacts.”

Authoritarian State Formation and State Collapse

Since de-globalization is accompanied by the collapse of the global deficit economy, which will lead to the devaluation of the neoliberal debt mountain, the most severe economic and social dislocations, as they devastated large parts of the periphery in the form of debt crises and economic collapses in the neoliberal era, seem likely to occur in the centers as well this time. If the capitalist functional elites have no further method of delaying the crisis at their disposal, the crisis process, which has been advancing in stages from the periphery to the centers since the 1980s, would thus reach its logical end point. It is not only the USA, which is groaning under an absurd private and state debt burden, that is facing the economic abyss in view of the necessary turnaround in monetary policy on interest rates; it is precisely export-fixated economies such as that of the FRG that are highly dependent on the global deficit economy by means of their export surpluses, which in fact represent an export of debt – and which could now be hit particularly hard by de-globalization.

Thus, at first glance, a tendency that was already apparent in the final phase of the neoliberal era seems to be advancing to become a central moment of the new crisis period: The state as an economic actor, which in recent years seemingly stabilized the system with stimulus packages and excessive money printing in the context of the last great liquidity bubble, is likely to become a central actor in the new crisis period.[42] The state, which seemingly stabilized the system in recent years with economic stimulus packages and excessive money printing in the context of the last great liquidity bubble, is likely to become the dominant economic actor in the short term due to the new quality of the crisis process – even if these state capitalist reflexes no longer have any prospect of success.

In general, the capitalist state, which already in its absolutist early form in the context of the European “economy of firearms” (Robert Kurz) acted as the most important impulse generator of the initialization of the valorization process, acts as a central economic actor in times of war and crisis. The state is not an alternative to the market, as it often appears in the truncated critique of capitalism, but a necessary corrective to the blind market dynamic, which tends to be auto-destructive. As soon as the contradictions inherent in capital valorization shake the system to its foundations through crisis or war, the state – which is always a capitalist state – must intervene to try to stabilize the system. Most recently, for example, in the period of crisis and war in the 1930s.

Even at present, in the face of climate crisis and war, there are voices calling for an open transition to rationing,[43] to state capitalism, to the war economy.[44] The state is not only supposed to support the “economy” through stimulus programs, the development of the new, “ecological” infrastructure and money printing, as in the final phase of neoliberalism; the state is also expected to be responsible for costly basic research, the subsidization of consumption or production and the organization of commodity distribution in phases of crisis. Strategic state decisions on industrial development are already part of bourgeois policy, for example in the FRG in the form of the promotion of “industrial champions” who are to conquer the world markets with state backing (here too the West is actually only following China and Russia).[45] Also foreseeable are, in reaction to coming crises, renewed nationalizations, especially in the ailing and crisis-prone late capitalist infrastructure sector.

This necessary role of the state as “crisis manager” is, however, undermined by the previously described exhaustion of the financial market-driven globalization of the deficit economy in the neoliberal age, which, in the face of dizzying mountains of debt, overheated financial markets and rapidly increasing inflation, drives politics into a dead end, a crisis trap: On the one hand, capitalist crisis policy should actually lower interest rates, print money and support the economy with stimulus programs in order to minimize the economic consequences of the war in Ukraine, but at the same time it would be necessary to raise interest rates and pursue a consistent austerity course in order to get at least some control over inflation.

This crisis trap, which is becoming ever clearer,[46] and marks the end of the credit-financed neo-liberal delay of the manifest breakthrough of the crisis in the centers, will, when it snaps shut, entail the most severe economic and social dislocations – especially in the centers, and especially in their middle classes. With the wave of impoverishment, the gradual brutalization of the bourgeois metropolitan societies, which has been going on for decades, will turn into open barbarization, driven by an escalating crisis competition at all levels, driving it into the anomic. The crisis-induced socio-political retreat of the state will reduce it to its original role as an instrument of repression. The new crisis thrust will thus entail a corresponding state reaction. Authoritarian state aspirations, present in neoliberalism in the form of the dismantling of democracy and the expansion of the surveillance state, will become openly apparent. The right-wing US President Trump was only a prelude in this respect. And in the Federal Republic, too, the latently fermenting fascist potential is only likely to become fully manifest when the civilizing effect of the high foreign trade surpluses, which compel Germany’s economic and political elites to take account of foreign opinion, disappears in the course of the crisis.

The war over Ukraine in particular makes this interaction of crisis dynamics, brutalization and authoritarian state reflex clear. Lukashenko, once called “Europe’s last dictator,” seems to be the forerunner of all those authoritarian tendencies that are currently spreading in the EU, for example in Hungary or Poland, in NATO, especially in the form of the Islamo-fascist regime in Turkey, or in Ukraine itself, which is already following in Russia’s footsteps with arrests of opposition members and party bans.[47] It is a fundamental mistake to interpret the war in Ukraine as a struggle between democracy and dictatorship, a view which could actually be corrected just by looking at the conditions in Warsaw, Budapest or Ankara. Consequently, the new phase of the crisis is more likely to be marked by the Orwellian struggle of authoritarian or fascist regimes for resources than by a new edition of the “Cold War.”

And yet this tendency towards authoritarian, and in the final analysis openly fascist, crisis management is a surface phenomenon, only externally linked to 20th century fascism. Total and totalitarian mobilization during World War II made the postwar Fordist boom possible, since there was effectively no demobilization after the end of the war and mass tank production passed into the automobilization, the mass production of cars, of postwar capitalist societies; but a similar regime of accumulation in which mass wage labor would be valorized in commodity production is not in sight this time. There is only the abyss of total over-indebtedness in the incipient climatic catastrophe, which gives a different course to the objective function of fascism as a terrorist crisis form of capitalist rule. The moment of fascism that has always existed as the rule of the rackets, that is, of competing communities of looters, as Critical Theory clairvoyantly stated, becomes dominant in the current systemic crisis.

The authoritarian formation of the state, which is increasingly becoming the prey of rackets, thus goes hand in hand with its internal erosion, which is already beginning to unfold in the Federal Republic in particular: especially with regard to the increasing right-wing extremist activities in the state apparatus.[48][49] In Ukraine this process has already progressed much further, where the oligarch rule after the fall of the government and the outbreak of the civil war already turned into right-wing extremist militia formation,[50] which could openly challenge the Ukrainian state in the run up to the war.[51] The disastrous course of the Russian invasion also revealed how far the tendencies towards state erosion had progressed even within the Russian state oligarchy, since even the army, essential for the Kremlin’s projection of power, was fully caught up in this. The division within the German right, which cannot clearly position itself behind the Ukrainian Nazis or Russian pre-fascism in the Ukraine war, points precisely to the omnipresence of these authoritarian-anomic tendencies in this conflict.[52]

A prime example of the fragility of authoritarian rule in capitalism and the transformation of dictatorship into anomie is provided by the Arab Spring, in the course of which seemingly monolithic dictatorships such as those in Syria and Libya collapsed and released their inherent centrifugal forces. Authoritarian structures are not a sign of the inner strength of the capitalist system, which prefers the optimization of the self-valorization of the wage-dependent within the framework of capitalist democracy, but rather its form of crisis, which is nowhere near as efficient at organizing the process of valorization as the typical published discourse in the centers of the world system on ways to optimize and increase growth – but which requires a certain degree of social stability to ensure its ideological foundations.

Amok or Emancipation

The era of openly authoritarian crisis management, which is now being heralded, for example, in the publicly articulated preference of Western oligarchs for right-wing populists,[53] will therefore not be able to bring about a decade-long post-war order in domestic politics either, as it prevailed at least in the centers during the neoliberal era, despite all the creeping processes of erosion and the increasing contradictions. The climatic, economic and geopolitical crisis impacts are coming with increasing frequency, which is why stabilization, which would herald a new historical period of crisis management, is hardly likely, even by means of authoritarian, dictatorial methods. Especially since, as already mentioned, the different moments of the crisis process are increasingly interacting, so that the climate crisis, for example, will have a growing economic and social fallout. The time of the monsters, as Gramsci called the breakthrough crisis to Fordism in the 1930s, no longer seems to have an end in sight.

It could even be argued that – with crisis imperialism and fascism striving towards the anomic as an open death cult[54] – in the phase of capital’s decline, moments of its expansionary dynamics briefly reappear, overlap, interact – entirely in the sense of a dialectical negation of negation, so that seemingly familiar phenomena at a higher stage of the capitalist development of contradiction follow a reversed logic of development driven by the contraction of the valorization process. These are blood-soaked early capitalist mementos from the ascendant phase of capital that the world system, which is passing into agony, once again unleashes upon humanity. Even the mercenary, who is currently celebrating a comeback in the neo-imperialist wars of distribution and collapse, is a product of early capitalism, when the first “wage earners” emerged en masse in the 30 Years War as an embryonic form of the wage-earner and terrorized the population.

Without an emancipatory overcoming of capital in its blind fetishistic flight towards world destruction,[55] the crisis has its final vanishing point in panic, in the capping of all libidinous bonds between the members of society triggered by escalating crisis competition, as already evidenced by the case of the individual run amok, which now occurs regularly.[56] In addition to global nuclear war, which is becoming an ever greater threat in crisis imperialism as the intensity of the crisis increases, it is the climate crisis that is likely to act as the greatest producer of panic: Specifically, the increasingly apparent uninhabitability of vast swaths of the global south,[57] which places objective limits on all, even the most brutal, openly terrorist forms of crisis management. This would mark the transition to sheer civilizational collapse.

From this systemic urge towards self-destruction, which is now blatantly obvious, grows the necessity of survival of the emancipatory overcoming of capital, which forms, so to speak, the last constraint with which the capitalist regime of constraint must be transformed into history. The struggle for the transformation of the system should thus be the central moment of left practice, instead of losing oneself in the jubilant cheering for NATO or Putin, which large parts of the German left are currently practicing in view of the Ukraine war.[58]

[1] https://oxiblog.de/die-mythen-der-krise/

[2] http://www.konicz.info/?p=4136

[3] https://www.xn--untergrund-blttle-2qb.ch/wirtschaft/theorie/stagflation-inflationsrate-6794.html

[4] https://de.wikipedia.org/wiki/Gro%C3%9Fer_Kladderadatsch

[5] https://www.heise.de/tp/features/Freihandel-und-Fluechtlinge-3336741.html

[6] https://www.mandelbaum.at/buch.php?id=962

[7] https://www.xn--untergrund-blttle-2qb.ch/wirtschaft/weltfinanzsystem-finanzmaerkte-notenbanken-6360.html

[8] https://www.xn--untergrund-blttle-2qb.ch/kultur/film/george_andrew_romero_zombie_4234.html

[9] https://www.xn--untergrund-blttle-2qb.ch/wirtschaft/theorie/stagflation-inflationsrate-6794.html

[10] https://www.mandelbaum.at/buecher/tomasz-konicz/klimakiller-kapital/

[11] https://www.xn--untergrund-blttle-2qb.ch/politik/theorie/die-klimakrise-und-die-aeusseren-grenzen-des-kapitals-6832.html

[12] https://www.lunapark21.net/das-kapital-als-weltverbrennungsmaschine/

[13] https://carnegieendowment.org/chinafinancialmarkets/86397

[14] https://www.co2.earth/daily-co2

[15] https://www.imf.org/-/media/Files/Publications/WEO/2022/April/English/text.ashx

[16] https://www.spiegel.de/wirtschaft/iwf-ukrainekrieg-kann-weltwirtschaftsordnung-fundamental-aendern-a-af821a51-222d-42d2-9038-d29180574e3d

[17] http://www.konicz.info/?p=4876

[18] https://www.dw.com/en/high-fertilizer-costs-threaten-farmers-amid-sanctions-on-russia/a-61163444

[19] https://www.reuters.com/business/indonesia-seeks-balance-international-local-palm-oil-demand-official-2022-05-11/

[20] https://twitter.com/spectatorindex/status/1525327269707022336

[21] https://www.heise.de/tp/features/Die-Urspruenge-der-gegenwaertigen-Wirtschaftskrise-4285127.html

[22] http://www.konicz.info/?p=1409

[23] https://www.heise.de/tp/features/Der-Aufstieg-des-deutschen-Europa-3370752.html

[24] https://lowerclassmag.com/2021/04/13/oekonomie-im-zuckerrausch-weltfinanzsystem-in-einer-gigantischen-liquiditaetsblase/

[25] https://www.heise.de/tp/features/Politik-in-der-Krisenfalle-3390890.html

[26] https://www.xn--untergrund-blttle-2qb.ch/politik/europa/russland-ukraine-krise-konflikt-neoimperialismus-6830.html

[27] https://www.ft.com/content/e5735375-75df-4859-bbf0-ae22e4fe2ff6

[28] http://www.konicz.info/?p=4389

[29] https://www.versobooks.com/books/347-adam-smith-in-beijing

[30] https://www.washingtonpost.com/news/wonk/wp/2015/03/24/how-china-used-more-cement-in-3-years-than-the-u-s-did-in-the-entire-20th-century/

[31] https://www.heise.de/tp/features/Wachstum-der-Schuldenberge-3762292.html

[32] http://www.konicz.info/?p=4643

[33] https://oxiblog.de/klimakrise-und-china/

[34] https://www.buzzfeednews.com/article/kirstenchilstrom/china-flooding-photos

[35] https://www.youtube.com/watch?v=DOBntnuYCMA&t=5s

[36] https://unherd.com/2022/03/the-truth-about-ukraines-nazi-militias/

[37] http://www.konicz.info/?p=4566

[38] https://www.streifzuege.org/2021/das-globale-agrarsystem-wahnsinn-mit-methode/

[39] https://www.tagesschau.de/ausland/asien/sri-lanka-ausnahmezustand-101.html

[40] https://www.heise.de/tp/features/Ost-oder-West-3363061.html

[41] https://ipad.fas.usda.gov/rssiws/al/crop_production_maps/Ukraine/Ukraine_wheat.jpg

[42] https://lowerclassmag.com/2021/04/13/oekonomie-im-zuckerrausch-weltfinanzsystem-in-einer-gigantischen-liquiditaetsblase/

[43] https://www.ft.com/content/d8e565b0-c769-46cc-9be3-4ed9a806d8e8

[44] https://www.spiegel.de/wissenschaft/mensch/ukraine-krieg-und-gas-dann-eben-kriegswirtschaft-aber-richtig-kolumne-a-532bb9fa-15e4-4b9b-8e50-d6e082a93f04

[45] https://www.zeit.de/wirtschaft/2019-05/nationale-industriestrategie-2030-peter-altmaier-industriepolitik-faq

[46] https://www.heise.de/tp/features/Politik-in-der-Krisenfalle-3390890.html

[47] http://www.konicz.info/?p=4832

[48] https://www.heise.de/tp/features/Braun-von-KSK-bis-USK-4355668.html

[49] https://www.heise.de/tp/features/Inflation-der-Einzelfaelle-4259590.html

[50] https://www.streifzuege.org/2014/oligarchie-und-staatszerfall/

[51] https://consortiumnews.com/2022/03/04/how-zelensky-made-peace-with-neo-nazis/

[52] https://www.endstation-rechts.de/news/die-deutsche-rechte-und-ihr-umgang-mit-dem-krieg-der-ukraine

[53] https://winfuture.de/news,129707.html

[54] https://www.heise.de/tp/features/Der-alte-Todesdrang-der-Neuen-Rechten-4509009.html

[55] https://www.heise.de/tp/features/Die-subjektlose-Herrschaft-des-Kapitals-4406088.html

[56] https://www.heise.de/tp/features/Fluchtpunkt-Amok-3263142.html

[57] https://www.spiegel.de/wissenschaft/mensch/extremwetter-und-klimaforschung-klimakrise-macht-hitzewellen-in-indien-100-mal-wahrscheinlicher-a-aa4a67a0-96f2-4be0-911f-a83f33abcaec

[58] Read more: https://www.konicz.info/?p=4868.

Originally published on konicz.info on 05/24/2022

{kind=link}